Context: Over 52 crore loans worth more than 32 lakh crore rupees have been sanctioned under Pradhan Mantri Mudra Yojana since the launch of the scheme in 2015. Half of the beneficiaries belong to SC, ST and OBC communities, and over 70% of them are women.

Pradhan Mantri MUDRA Yojana (PMMY)

1. Overview

Launched on: April 8, 2015

Scheme Type: Central Sector Scheme

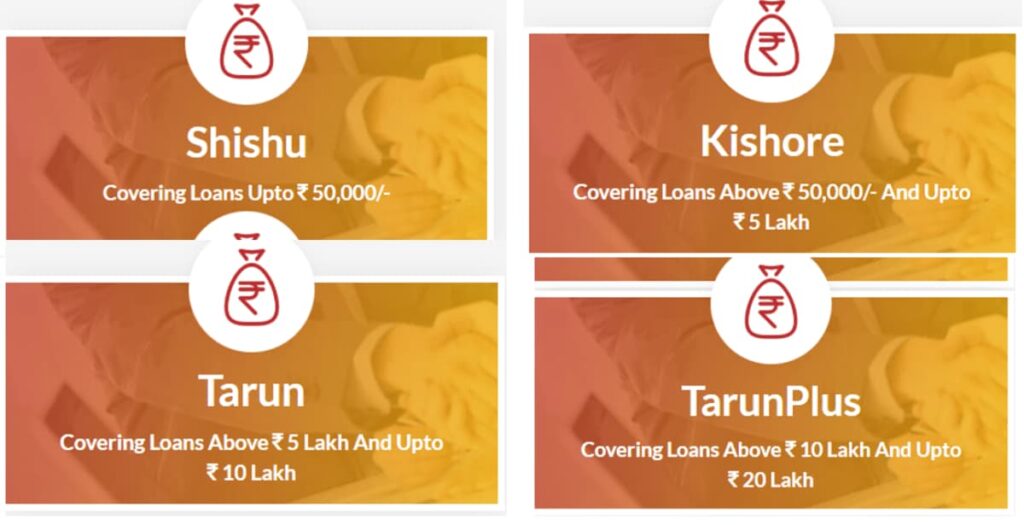

Objective: To provide loans up to ₹10 lakh to non-corporate, non-farm small/micro enterprises.

Loans under this scheme are classified as MUDRA loans.

2. Eligible Lending Institutions (Member Lending Institutions – MLIs)

Public Sector Banks

Private Sector Banks

State-operated Cooperative Banks

Regional Rural Banks (RRBs)

Micro Finance Institutions (MFIs)

Non-Banking Finance Companies (NBFCs)

Small Finance Banks (SFBs)

Other financial intermediaries approved by Mudra Ltd.

3. Eligible Borrowers

Individuals

Proprietary Concerns

Partnership Firms

Private Limited Companies

Public Limited Companies

Any other legally recognized entity

4. Application Process

Applicants can apply online via the portal:

👉 www.udyamimitra.in

5. Interest Rate

Interest rates are set by the Member Lending Institutions (MLIs).

Rates are determined based on RBI guidelines and may vary from time to time.

Components of MUDRA loans

- The scheme has been classified as:

Updates & Key Facts: Pradhan Mantri MUDRA Yojana (PMMY)

1. New Update: Tarun Plus

Effective from FY 2024–25, the upper cap for Tarun category loans has been increased from ₹10 lakh to ₹20 lakh.

This benefit is available at the discretion of banks and only for borrowers with a good repayment history.

The introduction of Tarun Plus has been a significant factor behind the increase in loan quantum disbursed under PMMY.

2. About MUDRA

MUDRA (Micro Units Development and Refinance Agency) is a refinancing institution under the Government of India.

It does not lend directly to micro-entrepreneurs or individuals.

Instead, it provides refinance support to eligible lending institutions such as banks, MFIs, NBFCs, etc., which then extend credit to small borrowers.

3. Present Status of MUDRA Loans

All-Time High Disbursal:

As of Q3 of FY 2024–25 (ending December 2024), MUDRA loan disbursals reached a record ₹3.39 lakh crore.

Top Performing Institution:

State Bank of India (SBI) holds the largest share in disbursing loans under PMMY.

Improved Asset Quality:

Non-Performing Assets (NPAs) under PMMY have shown a significant decline, falling from 4.9% in 2019–20 to 3.4% in 2023–24.

Benefits of MUDRA Loans

1. Financial Inclusion

Extends formal financial services to traditionally underserved groups, including:

Small entrepreneurs

Micro-enterprises

Self-employed individuals

Provides funding support to start, expand, or modernize operations, bridging the credit gap at the grassroots level.

2. Economic Growth

Enhances productivity and profitability of micro and small enterprises.

Plays a vital role in stimulating local economies and contributing to national economic growth.

3. Employment Generation

Supports the growth of small businesses and self-employment ventures, especially in rural and semi-urban areas.

Leads to job creation and fosters a culture of entrepreneurship.

4. Skill Development

Promotes skill building and capacity enhancement among micro-entrepreneurs.

Encourages individuals to enter trades and businesses with improved capabilities and confidence.

5. Women Empowerment

Encourages financial independence and entrepreneurship among women.

Helps promote gender inclusion in economic activities through targeted financial support.

Challenges and the Way Forward

Over-indebtedness among borrowers remains a concern, especially when repayment capacity is not thoroughly assessed.

There is a need for a comprehensive support ecosystem, including:

Financial literacy

Market linkages

Mentoring and business development services

Strengthening support systems and expanding the scheme’s reach will enhance its impact on inclusive development and sustainable economic growth in India.